LIFE ON THE FRONTLINE

LIFE ON THE FRONTLINE

Helping people navigate the financial nightmare

When I look back at the past seven years working as a Financial Mentor (FM) for a local budget service, things have changed dramatically. We’ve gone from seeing clients who just need a little coaching in money management, and people caught up in irresponsible lending, to desperate people who work long hours on minimum wage and still can’t make their budget balance. There’s always a deficit and often out of control debt. This happens because they don’t earn enough to have savings and when the car breaks down or some unexpected expense looms up, they have no reserves and have to borrow. Usually at high interest rates. Some who have Kiwisaver funds are so desperate they have to raid it just to make ends meet.

In June 2023 then National Party leader Chris Luxon said in a speech to Parliament that “We have 430,000 Kiwis now not able to pay their debts, and families are using budgeting services because they want to keep their homes and they now have to magic up $700 a fortnight just to pay the interest rates.” It’s interesting that Luxon singled out home owners for this statement, as if he’s their champion riding in on a white horse to save them. He’s not nearly so supportive of the chronically poor, the people he calls “bottom Feeders”, the ones who struggle daily to put food on the table for their kids. In my opinion he subscribes to the view a 2011 NZ Values Survey Report found, where “Around two-thirds believed people were poor because of personal deficits and they were generally not in favour of any increase in government assistance to them.”

Too often people view poverty from their personal standpoint so they can’t understand how it is for those struggling at the lower end of the economic scale. First Nations peoples have a proverb which says which defines empathy; “Never judge a person until you have walked a mile in their moccasins.” This is the mantra I live by as an FM. Our clients are people from all walks of life, from small business owners to workers, from home owners to renters and the homeless, from a variety of ethnicities, often with cultural obligations, and with a variety of competencies in the English language and financial literacy. They all have one thing in common, they need help navigating the financial nightmare they’re stuck in. The last thing they need is someone with a judgemental attitude coming along and telling them it’s their fault.

In an excellent article by Simon Wilson in the Herald on June 4, 2024, he said, “National and Labour, differ in many ways, but on one thing they are united: both are addicted to promising us we can have low taxes and a high level of public services: better hospitals, better transport, more police. So they compete to be the best at making that fantasy seem convincing. And then they can’t deliver.” He goes on to say that we need a circuit breaker and that we have a choice between the neoliberal ideal of Singapore (low tax and small welfare system) to the Scandanavian ideal of high taxes and superior infrastructure and social services. It’s interesting that Singapore’s outgoing PM Lee Hsien Loong repeatedly said of the need for increased social services, “If you can’t afford it, you can’t have it.” The reason being of course, the low taxes. Matthew Hooten writing on his Patreon blog said, “I prefer SIngapore but would be quite happy with ‘Scandinavia’ if that were the consensus. The main thing is to choose one and get on with it rather than remain stuck in the middle as we have been since 1999.” I know which one I’d choose.

Given that Luxon, in the lead up to the election, talked a lot about visiting foodbanks and budgeting services and how essential they were, you would think he might have boosted funding for them. Instead in April 2024, people working for budgeting services throughout Aotearoa got a nasty surprise. MSD cut the funding for a third of them, as well as all four debt solution services. They put the rest of the budget services on notice that future funding would not eventuate. I suspect Luxon was only at the various budgeting services for the photo ops, a chance to portray himself as someone who cares when he really doesn’t. A bit like promising to fund cancer drugs to get votes when he had no intention of actually funding them.

Nothing his government has done so far has made a positive difference to our clients’ lives. On the other hand, the coalition has done a lot to make them a lot tougher, and Willis’s no-frills budget has only added to that.

Beneficiary bashing is a favourite of right wing governments and this one is no different. Wilson also added in his article, that “The Budget retains the $50m or so the Government spent last year investigating benefit fraud, although it generated only the same amount in savings. White-collar crime, on the other hand, is a $7 billion activity. But the Serious Fraud Office gets a mere $17m a year to fight it, an amount that remained static in the Budget.”

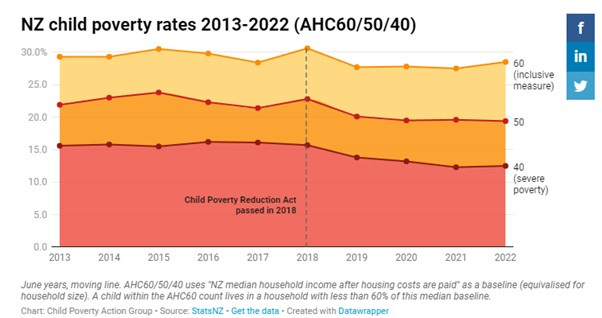

WIllis’s comment when asked how would beneficiaries benefit from the budget was, “Get a job”. Only someone from a well-off privileged background would make such a smug comment. Most of the clients we see have jobs and when it takes one wage to pay rent and the other to pay for everything else, you can see how easy it is to end up in a debt spiral. At least the government measures poverty now, and for a while it was trending down but in a report from the Child Action Poverty Group the latest figures from Stats NZ indicate they are all trending up again.

In an RNZ interview, after the announcement of the cuts to budget services, MSD spokesperson Mark Henderson said that “People could still get support from a range of government-funded services to help improve financial wellbeing and reduce debt.” But can they, and how do they find them. He also said in another interview That “The government decided to fund a certain number of staff from 1 July, replacing the existing model of funding client sessions. The new model gives providers greater flexibility to tailor services to client's needs.”

Budget services have always tailored their services to client’s needs. FMs are highly trained and experienced so we know how to navigate the minefields our clients get caught up in. We don’t just do budgets, and sessions are merely a record of the face to face visits with clients. Most of the work is done on behalf of clients. Sessions hardly cover even 10 percent of the work we do. The hours on the phone, emailing, photocopying, negotiating, consulting other FMs, researching the law and how it might apply to our client’s problem, following up, analysing bank statements, and creating arguments to challenge irresponsible lenders.

Often cases require in-depth knowledge of consumer credit law, employment law, tenancy law and the CCCFA has been a godsend allowing us to finally get some wins against irresponsible lenders. In our service only our part time co-ordinator is funded as well as a small budget for marketing. The rest is all done by overworked volunteers.

Fincap released its Voices Report in May this year and it makes sobering reading. Financial mentors supported more whānau with the number increasing from 49,568 in 2022 to 69,807 in 2023. And we did that with fewer FMs. The four hours per week we were rostered on as volunteers, ballooned out to four to eight a day. MSD had already cut funding to the sector and then they did it again, no doubt at the behest of Willis and her cost slashing directives.

I checked Mark Henderson’s statement by logging in to the government website which said, for people needing help to call the Money Talks helpline, talk to a Financial Mentor, or join a MoneyMates support group. Money Talks is contactable by phone, text, email and via their website chat. Generally, they refer callers to a budgeting service. They run Facebook groups like Cheaper Living and Money Talks on Facebook. Other government funded entities like Sorted have tools, calculators, and a wealth of information. Sorted works well for financially literate people, always provided English is their first language. Anyone else, not so much.

I found a programme run by the Retirement Commission for Māori and Pasifika people, but how would they know where to access it. Online help is predicated on people being able to navigate systems designed for financially literate, mostly English speaking people.

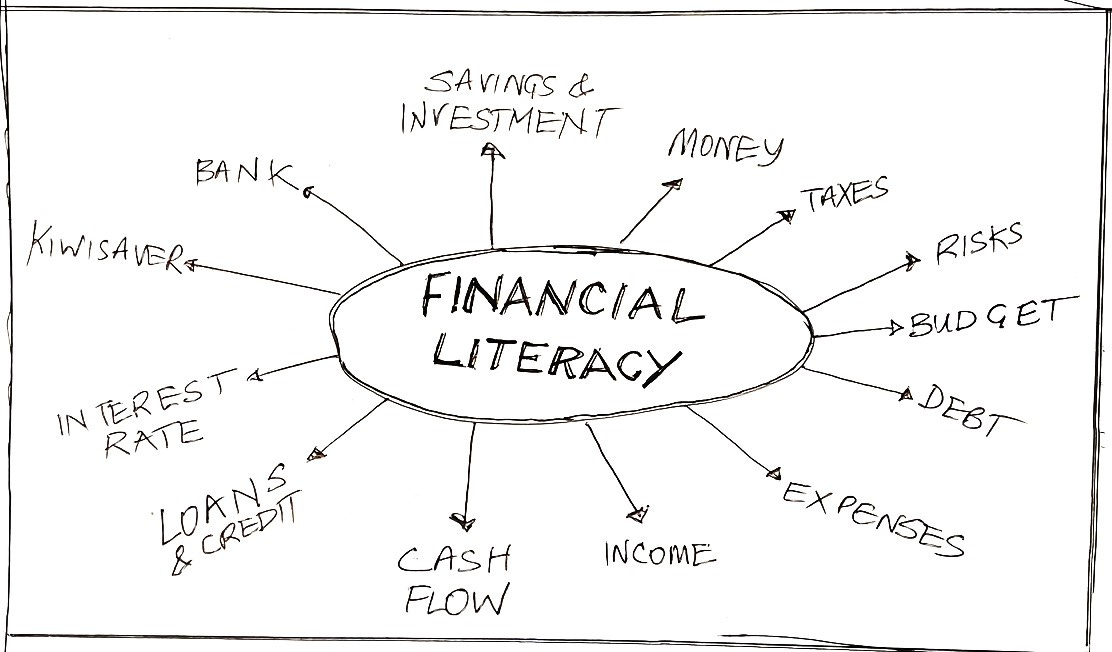

Something FMs up and down the country ask is, “why is financial literacy not taught in school”. We see so many young people caught up in unaffordable loans because they have no idea of what they’re getting themselves into. Not only that, but they also have no idea how to budget, or to manage their money. If you look at their bank statements, it’s a daily cascade of small payments for all sorts of things essential or not. There is no organisation. A savings account is constantly being raided to cover costs and if you ask them what they spend on food including takeaways, or fuel, they have no idea and always guess a figure much lower than the actual. Our budgeting service runs financial literacy courses for Springboard, an organisation which helps young people learn life skills and those who attend are grateful to learn about managing a budget. But unless NGOs are doing the training, it doesn’t happen.

In 2023 after a lot of lobbying, Labour announced a policy for the mandatory teaching of financial literacy in schools. National quickly jumped on the bandwagon promising to do it too. However, nowhere in the education budget is there anything that mentions teaching financial literacy.

I can hear some of you say, “where are the parents in this, how come they don’t teach their children.” The answer to that is most of their parents are in the same boat, they haven’t been taught either. Many clients, once we give them the basics and tools on how to budget are so much better off and they teach their kids too. But even quite savvy people running their own small businesses need help with budgets and spreadsheets and keeping a set of accounts.

As a society we are far to reliant on seeing everything through a white privileged lens. I get into trouble for saying this but it’s true. The comment from Mark Henderson is exactly that. It makes all kinds of assumptions that don’t translate into reality.

Every day our co-ordinator has new clients contacting the service seeking help and begs our overloaded FMs to take on yet another client. Because we know it makes a difference, we do it, but all of us are close to burn out and the numbers keep coming.

THank you Cheryl. That's great to hear. The best day for a Financial Mentor is when a client says, "I can manage on my own now." It's so satisfying and wonderful to see them get on top of their issues and make it work.

It would be good if they did read it. But I suspect that it doesn't fit with National's agenda for Social Investment and picking and choosing who they licence to operate under it. They've started it already with Mike King. The downside of picking one programme over another is that there is no overall plan and mental health is becoming a serious issue. Most of my clients are depressed and their mental wellbeing is being eroded daily simply by the hopelessness of it all. Scrapping the Fair Pay agreement and not increasing minimum wage is one of the worst things they could have done.

Labour are no better, sadly. They had a huge opportunity to do something transformative and they didn't.

To me I think it's time to get rid of both these legacy parties as they've become stale and stuck in outdated iseology.